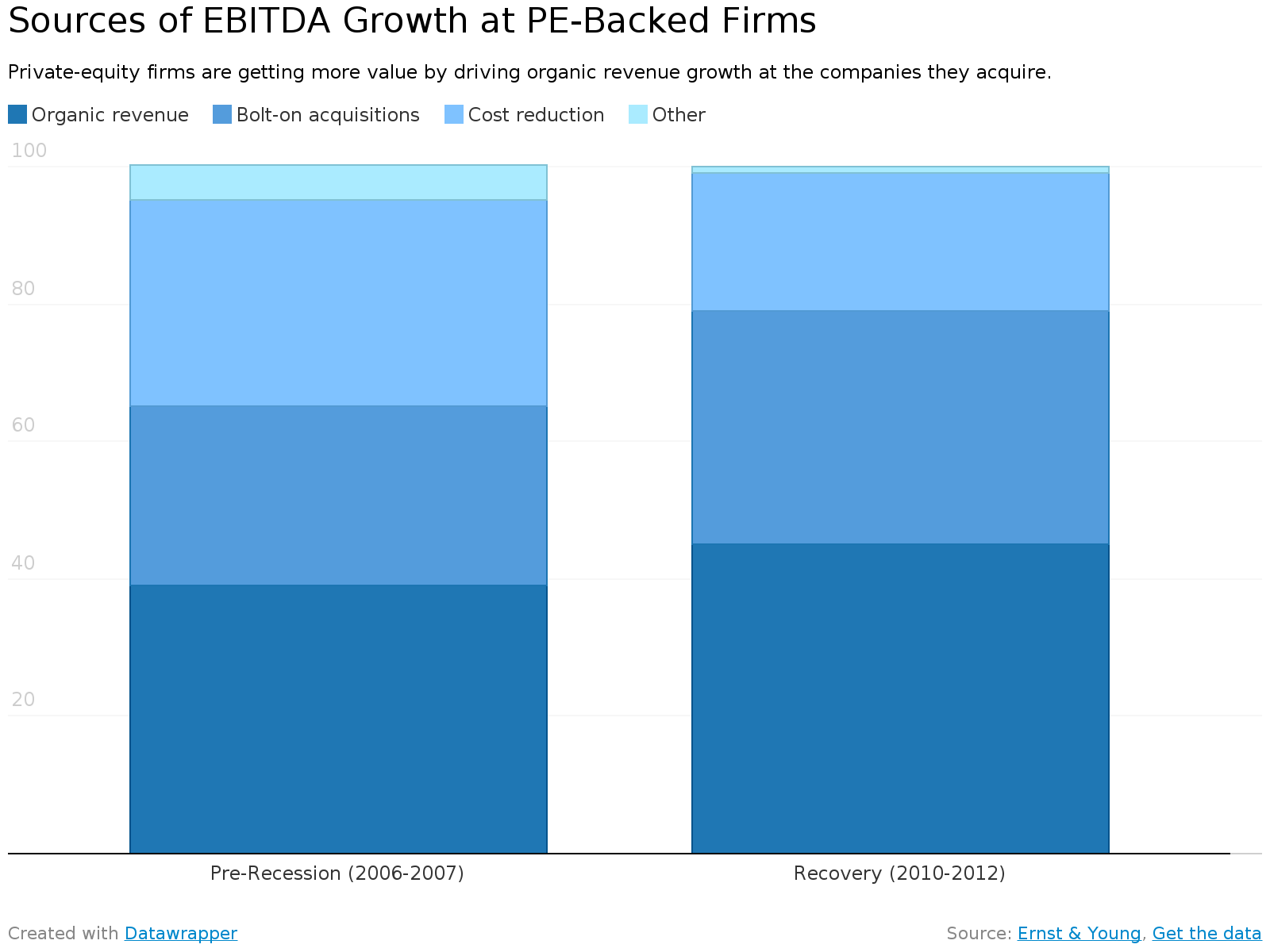

… but an E&Y study I wrote about yesterday claims they are creating value — with returns higher than the public markets — with some new “levers.” I’m not so sure. The businesses they have acquired are earning higher valuations on exit because the stock of their public-company peers is doing well. “Multiples, which compressed significantly during the post-crisis years and negatively impacted performance, have rebounded in the recovery period and accounted for 30 percent of overall PE returns,” the E&Y report says. And what about the value to the U.S. economy of all these high returns? PE firms are doing hordes of dividend recaps again, so the money is going to high net-worth and institutional investors. Is it driving jobs? Who knows.

Related articles

- Memo to the Eliot Spitzer: Private Equity Firms are Scamming New York City (nakedcapitalism.com)

- What’s Private Equity Good For? (blogs.wsj.com)

- Private Equity Exits Hit by Economic Uncertainty (pehub.com)

Leave a comment